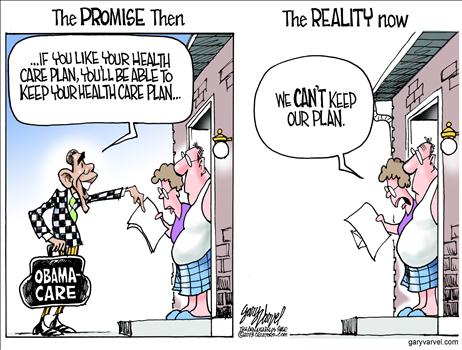

ObamaCare –Image Courtesy: Barracuda Brigade

ObamaCare –Image Courtesy: Barracuda Brigade

(Catholic Online) ObamaCare is scheduled to go into effect in 6 months–the key provision of the Obama Administration, the package is intended to mandate that individuals carry health insurance and require that health-benefit providers are spending at least 80% of premiums collected on health care for their insureds.

However in the State of California, three major health insurance providers (United Health Group, CIGNA & AETNA) are setting out of the state’s health insurance exchange. Why would these major insurance carriers decide to opt out of one of the largest insurance markets in the nation if there isn’t any inherent problems with how ObamaCare functions?

What do they know that you don’t?

The Motley Fool points out that the most optimistic scenario calls for around 5 million people to purchase health insurance through the California/ObamaCare Exchange–the flood of new insureds would enable those insurance carriers participating in the exchange to make money on higher volume while offering insurance at lower rates–Capitalism at its finest right?

A gloomier and more likely scenario is that a much lower number of people will purchase insurance through the exchange, possibly causing the insurance carriers participating to lose money because they based their rates on overly rosy assumptions.

While we won’t know which scenario will unfold for a while there are some cost comparisons to keep in mind. An individual may be able to purchase insurance through Kaiser for as little as $82 a month–but the state has an estimated 7 million people without health insurance. Even with subsidies, a 21 year old (who decides to opt out of her/his parents health insurance plan) making $35,000 annually will have to pay about $64 a month for the least expensive ObamaCare plan–around 2.6 Million residents will likely qualify for some level of federal subsidies, leaving around 4.5 Million currently uninsured with no financial subsidies–ObamaCare advocates believe these people will now run out and buy health insurance.

Riiight…

The other cost to keep in mind is $95 that is the penalty tax (for the entire year) that a person must pay to the IRS if she/he doesn’t buy health insurance. Will individuals pay $82 a month now for health insurance or will they go with the much cheaper penalty tax?

One other major fact to always keep in mind, under ObamaCare’s own rules, health insurance carriers can no longer decline to insure someone for pre-existing health conditions. How many young and healthy Americans will decide to decline purchasing health insurance now, pay the $95 annual penalty tax and only decide to go out and purchase a policy of health insurance when necessary?

While United Health, CIGNA & AETNA combined only represent about 7% of the total health insurance market, the message that these insurers are sending to California is much more important–these companies are still very skeptical as to how things are going to play out with the ObamaCare exchanges.

The State of California may offer a wealth of possibilities but its simply not worth the price of admission based on United Health’s decision to opt out of the ObamaCare exchange–a lack of large national insurance presence in California is only bound to increase mounting skepticism over how effective the exchange will ultimately be in manufacturing competition among insurers.

In return of a lack of of recognizable insurance names could diminish consumer interest in researching the health plans, which will defeat the entire purpose of setting up the ObamaCare exchanges.

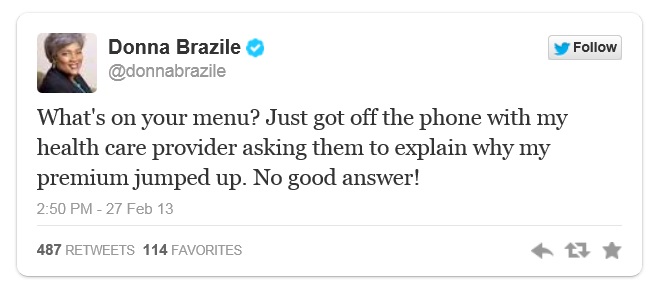

Former DNC Chief Tweets Health Ins Premium Hike –Expose The Media

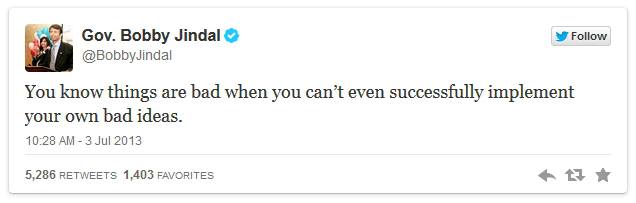

Former DNC Chief Tweets Health Ins Premium Hike –Expose The Media Gov Bobby Jindal on ObamaCare –Tweet Courtesy: Chicks On The Right

Gov Bobby Jindal on ObamaCare –Tweet Courtesy: Chicks On The Right

Stop & Spell –Image Courtesy: Teachers Paradise

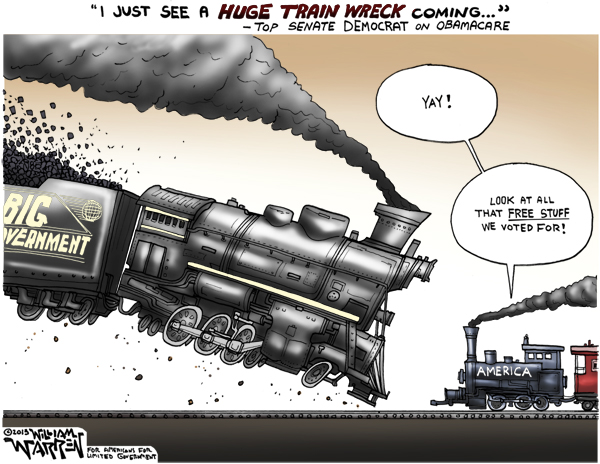

Stop & Spell –Image Courtesy: Teachers Paradise Train Wreck –Image: Net Right Daily

Train Wreck –Image: Net Right Daily Democrats Raid $716 Billion from Medicare to Fund ObamaCare

Democrats Raid $716 Billion from Medicare to Fund ObamaCare President Obama: Maybe You’re “Better Off” Taking Painkillers and Foregoing Surgery –Real Clear Politics

President Obama: Maybe You’re “Better Off” Taking Painkillers and Foregoing Surgery –Real Clear Politics